The Project Labor Agreement and Troubled Union Multiemployer Pension Plan Nexus

Construction unions attempt to entice merit shop craft professionals and new construction industry workers and apprentices into joining a union with promises of generous retirement benefits via multiemployer pension plans.

Construction unions lobby elected officials in charge of procuring taxpayer-funded construction projects with arguments on why union contractors and union workers deserve special treatment through various schemes like government-mandated project labor agreements, responsible contractor ordinances and union apprenticeship requirements because of the alleged public good provided to workers who participate in union-affiliated MEPPs, even though less than 13 percent of the U.S. private construction industry belonged to a union in 2018.

Amongst the many reasons why merit shop contractors and construction workers oppose PLA mandates, they typically require merit shop contractors to pay their workers’ retirement fringe benefits to union-affiliated MEPPs while working on a PLA project instead of into existing retirement plans. However, data continues to show that hundreds of union-affiliated construction industry MEPPs are in serious financial trouble, calling into question the validity of promises that a PLA will deliver a generous retirement benefit for employee participants.

The Employee Retirement Income Security Act of 1974 requires the Pension Benefit Guaranty Corporation—an independent agency of the federal government that monitors and privately insures pension benefits in private sector defined benefit plans such as MEPPs—to issue reports on an annual basis about the health of PBGC-backed plans.

Unfortunately, the PBGC’s FY 2018 Annual Report says, “We remain concerned… …regarding the Multiemployer Program not being able to meet its obligations before the end of FY 2025.”

In short, the PBGC risks certain future insolvency unless drastic changes are made to the MEPP program.

According to the to the PBGC’s 2015 Pension Insurance Data Tables, the Net Financial Position of PBGC’s FY 2016 Multiemployer Program had $2.2 billion in assets and $61 billion in liabilities, for a deficit of $58.8 billion, an all-time high for the MEPP program (see Table M-1). Likewise, according to a 2017 U.S. Government Accountability Office (GAO) report on MEPPs:

Since fiscal year 2013, PGBC’s financial deficits have more than doubled. At the end of fiscal year 2016, PBGC’s net accumulated financial deficit was over $79 billion—an increase of about $44 billion since 2013. At the same time, PBGC estimated that its exposure to future losses for underfunded plans was nearly $243 billion.[1] The single-employer program, composed of about 22,200 plans, accounted for $20.6 billion of PBGC’s overall deficit (see figure 21). The multiemployer program, composed of only about 1,400 plans, accounted for about $59 billion. According to PBGC, these dramatic increases were attributable to broad economic factors and financial conditions of the plans PBGC insures.

Troubled Construction Industry MEPPs Expose PBGC To Insolvency

At the beginning of 2014, PBGC-insured MEPPs had $466 billion in assets vs. $958 billion in liabilities, for an underfunding of $496 billion or a 48 percent funding ratio (see Table M-10).

Additional data from the PBGC indicates the construction industry is a key contributor to the drastic underfunding of MEPPs, and a likely cause of dramatic future PBGC insurance program funding shortfalls:

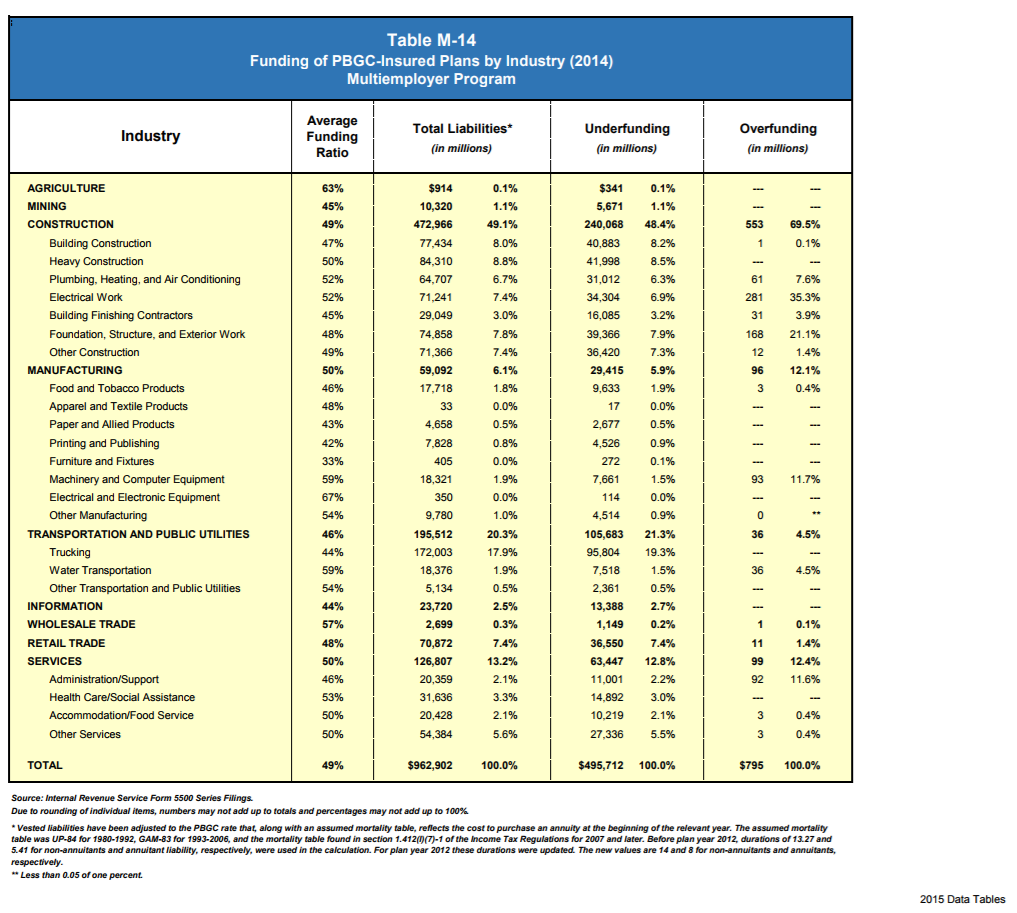

- According to the PBGC’s 2015 Pension Insurance Data Tables, which contains the most recent PBGC data on industry MEPPs, construction industry MEPPs are responsible for about $240 billion (or 48.4 percent) of all PBGC-insured MEPP underfunding, which totals $496 billion. (See Table M-14 below: Funding of PBGC-Insured Plans by Industry [2014] Multiemployer Program).

- The amount of the construction industry’s MEPP underfunding continues to get worse. In comparison, similar 2009 PBGC data found the construction industry was responsible for about $87.8 billion (or 45 percent) of PBGC-insured MEPP underfunding (see Table M-14: Funding of PBGC-Insured Plans by Industry [2007] Multiemployer Program). Table M-14 of the 2010 PBGC report indicates the construction industry’s portion of all PBGC-insured MEPP underfunding grew to $167 billion (or 47 percent) in 2009.

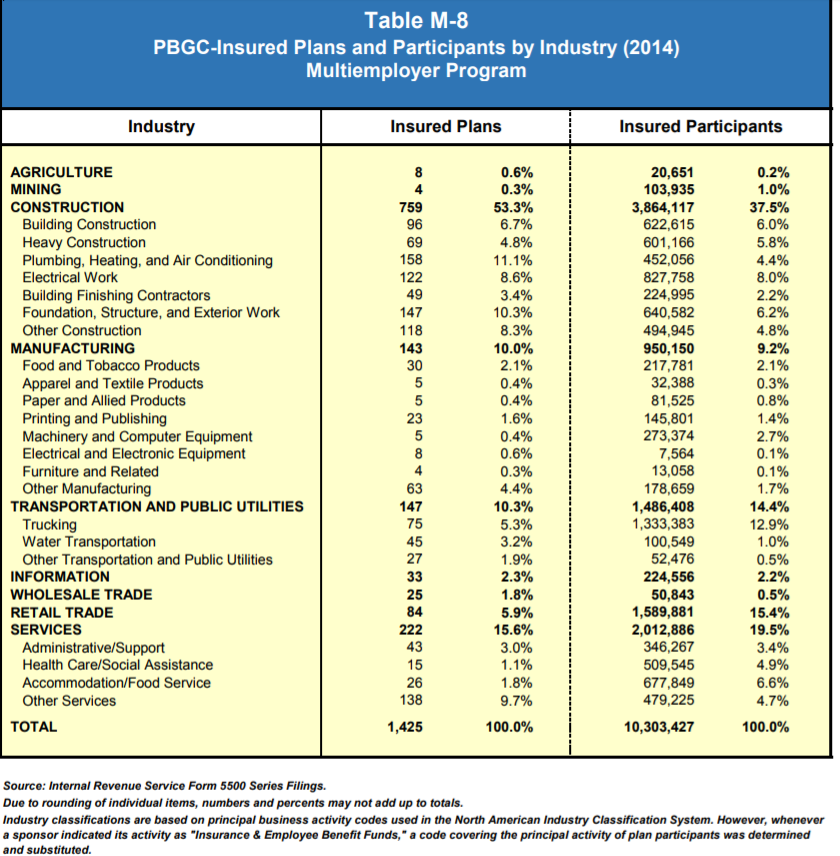

- Seven hundred and fifty-nine (53 percent) of the 1,425 MEPPs insured by the PBGC are in the construction industry. (See Table M-8 below: PBGC-Insured Plans and Participants by Industry [2014] Multiemployer Program).

- The construction industry has a total of $473 billion (49.1 percent) worth of the PBGC’s total liabilities. (See Table M-14 below: Funding of PBGC-Insured Plans by Industry [2014] Multiemployer Program).

- The largest number of employees from any industry, almost 3.9 million (37.5 percent) of the 10 million PBGC-insured MEPP participants (workers and retirees), is from the construction industry. (See Table M-8 below: PBGC-Insured Plans and Participants by Industry [2014] Multiemployer Program).

Expect the construction industry’s MEPP underfunding problem to continue to worsen, which will exacerbate future PBGC insolvency. Unfortunately, the public still doesn’t know the real-time financial implications of underfunding in 2019, thanks to a multi-year lag in the public reporting of the financial health of MEPPs.

Why Is the PBGC in Financial Trouble?

The PBGC has publicly raised concerns about the simmering funding crisis because its balance sheet is impacted by the health of MEPPs. Individual MEPP insolvency triggers the PBGC’s guarantee, and loans are provided to the MEPP by the PBGC to help it pay benefits to worker participants (up to $12,870 per year per individual beneficiary). PBGC financing comes from insurance premiums paid by companies insured by the PBGC, as well as other sources such as investment income, plan assets and other recoveries. Taxes and other sources of public financing do not fund the PBGC plans.

Should the PBGC insurance program become insolvent before 2025 as predicted, it is unclear what will happen to plan participants backed by the PBGC, but benefit cuts are likely.

As 2018 drew to a close, members of a special Congressional Joint Select Committee on Solvency of Multiemployer Pension Plans committee failed to deliver a package of reforms to save struggling plans, head off more plans running into trouble and shore up the PBGC multiemployer program. In the 116th Congress, lawmakers are currently offering bills to address the crisis, but many proposals have been accused of being a bailout at the expense of taxpayers and/or failing to address the fundamental structural flaws of MEPPs causing them to fail. Others argue the federal government has bailed out the private sector previously and is better off making a difficult decision now instead of later.

MEPPs in the Construction Industry

All MEPPs are defined by the Taft-Hartley Act of 1947 and cover workers from more than one employer. Employer contributions, determined by collective bargaining with a labor union, fund the plan. These plans exist to provide benefits to unionized workers in businesses characterized by frequent job and employer switching, such as union craftspeople in the construction industry. Under a plan, service with multiple employers is treated the same as if the worker had been with the same employer during the life of the employee’s career.

Unionized contractors receive craft labor from union hiring halls composed of tradespeople who specialize in a specific craft (e.g., IBEW dispatches electricians and LiUNA dispatches laborers). During their career, union workers may be dispatched by union halls to dozens of union-signatory contractor employers. Designated union bosses and union contractor representatives administer pension plans (plan trustees) that multiple union-signatory employers (contractors) must pay into on behalf of employed trade union members in accordance with their respective collective bargaining agreement(s) with a construction union.

In contrast, merit shop contractors typically hire, train and invest resources in tradespeople who work exclusively for the company in a traditional employee/employer relationship. These contractors typically provide benefits packages including a portable 401(k), paid time off, medical and dental insurance, training and profit sharing to attract and retain skilled, experienced employees in the free market.

Merit Shop Avoidance of MEPPs and PLA Mandates Justified

As TheTruthAboutPLAs.com has stated many times, one of the reasons merit shop contractors are discouraged from competing for taxpayer-funded contracts on construction projects subject to government-mandated PLAs is because of typical provisions in a PLA that require employers to contribute to union-affiliated MEPPs on behalf of employees for the life of the project.

In rare instances when nonunion employees (and union employees who do not belong to unions that are favored in PLAs) and their employers participate in PLA projects, employers must make hourly benefit contributions to union MEPPs on behalf of their employees. These benefit contributions are forfeited to the MEPP unless employees join a union and meet vesting schedules defined by each plan.

An October 2009 report by Dr. John R. McGowan, “The Discriminatory Impact of Union Fringe Benefit Requirements on Nonunion Workers Under Government-Mandated Project Labor Agreements,” found nonunion workers’ take-home pay is reduced by at least 20 percent when their employers enter into PLA arrangements containing a MEPP requirement. It also found a PLA mandate’s controversial double fringe benefit requirements has the potential to increase merit shop contractor labor costs by 25 percent, making it difficult, if not impossible to win contracts.

Besides confiscating benefits rightfully earned by construction employees working on a PLA project, PLA pension provisions are a windfall for unions’ MEPPs because the MEPPs don’t have to pay future benefits to those employees who have contributed but failed to meet vesting requirements. Though small in comparison to overall funding shortfalls, these contributions prop up insolvent plans and hide the flawed structure and Ponzi-scheme economics of many construction industry MEPPs.

For decades, merit shop firms have offered alternative retirement plans to their workforce that are portable and controlled by individuals because union-affiliated MEPPs simply cannot be financially sustained in the long term. Construction industry stakeholders have only publicly and aggressively addressed MEPP underfunding during the past decade, partially because of scrutiny from the financial industry.

Merit shop contractors should be extremely cautious about contributing to MEPPs, even on a PLA project where MEPP liability appears to be limited, because it can expose contractors to pension withdrawal liability for a share of the future liabilities of plan participants.

During the construction industry recession, many contractors participating in MEPPs went out of business. And when MEPP participants go belly up, the burden on employers remaining in the MEPPs becomes greater. Bankrupt contractors that can’t pay their fair share to MEPPs create additional liability for a MEPP’s remaining employer participants, which results in all sorts of disastrous consequences, such as forcing more employers out of business, weakening already struggling MEPPs, and compelling the PBGC to step in to provide benefits to MEPP beneficiaries at a reduced rate, which could trigger PBGC and MEPP insolvency.

The Blame Game

The recession’s peak industry unemployment rate of nearly 25 percent, a decline in construction industry union membership, industry demographic changes driven by retiring baby boomers and a looming construction industry workforce shortage point to future insolvency for many MEPPs.

In response, lobbyists representing union interests tried to exploit its political clout to fix its pension woes by pushing lawmakers, the U.S. Department of Labor and bureaucrats at the National Labor Relations Board to pass rules that will make it easier for unions to organize and add new members to the basement of their MEPP scheme (see the Workplace Democracy Act, Employee Free Choice Act/Card Check, Executive Order 13502, Ambush Elections, Micro Unions and Invasion of Privacy). Similar measures are sure to be reintroduced in a Democrat-controlled House but are unlikely to end up on the president’s desk with a GOP majority in the Senate in the 116th Congress.

In addition, unions have ratcheted up rhetoric blaming PBGC insolvency and their pension troubles on Wall Street and the recession, among others. Instead of pushing reasonable solutions identified by the Congressional Budget Office like adjusting benefits, increasing contributions, preventing fraud and waste, executing sound investment and management strategies, and diverting hundreds of millions of dollars of annual discretionary union political spending to shore up pension plans, some labor leaders are playing the blame game and posturing for loan, a bailout and/or a temporary band-aid from Uncle Sam.

However, the shaky financial condition of some MEPPs was obvious pre-recession and occurred under the watch of union pension trustees, such as this example from a TheTruthAboutPLAs post:

The Sheet Metal Workers National Pension fund discloses the plan’s annual funding levels for plan participants here. The SMWIA union’s own pension fund documents indicate that on Jan. 1, 2008, the fund was just 52.2 percent funded.

So just three months after the Dow closed at a then all-time high of 14,164 on Oct. 9, 2007, the pension fund took such a big loss in the stock market that the plan ended the year at 52.2 percent funded?

A July 26, 2009, article in The Wall Street Journal points to similar anecdotes of pre-recession MEPP underfunding in other industries, as well as inequality between the pension plans of rank-and-file members and union leadership:

Poor management probably deserves a lot of the blame for the decline in MEPPs, but there are many contributing factors. What’s troubling to some rank-and-file members and conservative pundits is that unions do a far better job with retirement funds created for their officers and employees than for membership. For example, the SEIU Affiliates, Officers and Employees Pension Plan—which covers the staff and bosses at its locals—was funded in 2007 at 102.2 percent. The plan for the folks at SEIU international headquarters was funded at 84.8 percent.

A September 2009 report on union pension plans by the Hudson Institute, “Comparing Union-Sponsored and Private Pension Plans: How Safe Are Workers’ Retirements?” found similar results and highlighted the disparities between union officer pension plans and union member plans. So does this piece.

Almost 10 years later, with the Dow nearly 10,000 greater, MEPPs remain in trouble and many union officer pension plans remain healthier than union member plans.

Get to Know Your MEPP

The U.S. Department of Labor provides a list of all troubled MEPPs here, and ERISA Sec. 101(f) requires MEPPs to provide an annual funding notice to participants.

In 2019, TheTruthAboutPLAs.com sorted through the growing list and identified construction industry MEPPs in this easy-to-search spreadsheet, where industry stakeholders can see if the MEPP they are participating in (or competitors pay into) is in trouble. In 2018, there were 148 plans in critical, endangered or critical and declining status. More than 1900 construction industry MEPPs have fallen into these trouled categories since 2008.

For too long, construction industry employees, contractors and lawmakers have been fooled into thinking union MEPPs deserve special treatment and are a safe retirement strategy. The truth is that many plans are in poor shape and were unhealthy even in the best of economic times. Some construction industry MEPPs have offered limited transparency, accountability or meaningful solutions to fix this problem. Construction workers should not be forced to contribute to MEPPs as a condition of employment on a PLA project. It is clear they might be better off participating in 401(k) plans and other safer retirement strategies. Without proper education, oversight and corrective action, workers, contractors and taxpayers should expect more problems from unsustainable MEPPs.

In the interim, the merit shop contracting community’s embrace of portable retirement plans controlled by workers and avoidance of government-mandated PLA requirements forcing contributions to MEPPs, will continue to be a viable strategy benefitting the construction industry workforce its employers and taxpayers.

Learn more about the health of MEPPs here.