Taxpayer Bailout of Multiemployer Pension Plans and Government-mandated Project Labor Agreements

On March 11, President Biden signed the American Rescue Plan Act of 2021 (H.R. 1319) into law, including a controversial provision providing a Congressional Budget Office-estimated $86 billion taxpayer bailout of struggling multiemployer pension plans.

The COVID-19 relief bill’s sudden bailout of some MEPPs has been disheartening to some small businesses and firms not affiliated with MEPPs, which are common with union-signatory competitors. For decades, firms not affiliated with unions have recognized the structural flaws of MEPPs and potential for costly MEPP withdrawal liability and plan insolvency.

“Small businesses work hard to provide good benefits for their employees and call the concession to these plans a costly bailout,” said Peter Comstock, senior director of legislative affairs at Associated Builders and Contractors in a March 11 interview with Construction Dive.

The funding injection is, however, welcome news for about one million workers in targeted MEPPs facing insolvency. Promised defined retirement benefits through collective bargaining between union representatives and MEPP union-signatory employer participants, these workers had no real chance of collecting the full pension amount promised due to a variety of systematic flaws in the MEPP system. The Pension Benefit Guaranty Corp., privately funded by investment returns and plan premiums paid by MEPP participants, protects insolvent MEPP participants with reduced defined benefits up to $12,870 per year in certain circumstances. However, the PBGC has only $3 billion on hand and is projected to run out of cash as early as 2025, mostly because its exposure to failing MEPPs.

MEPP funding relief advocates, union lobbyists and union-signatory contractor lobbyists argue that many businesses received COVID-19 relief, so why shouldn’t MEPP retiree participants? In contrast, watchdogs point to the fact that many of these plans have been in trouble for decades, well before the COVID-19 pandemic disrupted the economy, although the pandemic’s recession certainly didn’t help. The true cost of this bailout is likely to grow even more than anticipated, depending on forthcoming regulations implementing the plan.

Watchdogs and newspaper editorial boards have almost universally agreed on one fact: the COVID-19 relief bill’s taxpayer-funded cash infusion into struggling MEPPs will not fix the underlying MEPP flaws and the public should prepare for another bailout in the future unless additional legislation fixing MEPP structures is passed.

More from a Washington Post Feb. 17 editorial:

“For years, Republicans and Democrats have tried to negotiate a package to protect workers without soaking taxpayers—most of whom do not even have defined-benefit pensions. Proposals have generally involved some combination of benefit trims, greater employer insurance premiums and federal support. Yet the bill just approved by Ways and Means one-sidedly provides the funds a slug of federal cash, with little structural reform required beyond a somewhat increased employer premium. Its likely net cost: $86 billion.

“To make this pension bailout fit within the $1.9 trillion budget ceiling suggested by Mr. Biden and enshrined in a budget reconciliation resolution, along with $1,400 stimulus ‘checks’ and other spending items, the committee had to offset the cost by ending a much more vital program—extended unemployment benefits—at the end of August rather than September, as Mr. Biden originally advocated.”

The Wall Street Journal wrote in a Feb. 21 editorial, “The Non-COVID Spending Blowout”:

“The bill includes $86 billion to rescue 185 or so multiemployer pension plans insured by the Pension Benefit Guaranty Corp. Managed jointly by employer sponsors and unions, these plans are chronically underfunded due to lax federal standards and accounting rules. Yet the bailout comes with no real reform.”

The New York Times March 7 article, “Rescue Package Includes $86 Billion Bailout for Failing Pensions,” explains problems with the bailout:

“Both the House and Senate stimulus measures would give the weakest plans enough money to pay hundreds of thousands of retirees—a number that will grow in the future—their full pensions for the next 30 years. The provision does not require the plans to pay back the bailout, freeze accruals or to end the practices that led to their current distress, which means their troubles could recur. Nor does it explain what will happen when the taxpayer money runs out 30 years from now.

Using taxpayer dollars to bail out pension plans is almost unheard-of. Previous proposals to rescue the dying multiemployer plans called for the Treasury to make them 30-year loans, not send them no-strings-attached cash. Other efforts have called for the plans to cut some people’s benefits to conserve their dwindling money — such as widow’s pensions, early retirement subsidies and pensions promised by companies that subsequently left their pools.

While companies that run their pension plans solo must follow strict federal funding rules, multiemployer plans do not have to. Instead, the companies and unions hammer out their own funding rules in collective bargaining. Both sides want to keep the contributions low — the employers to reduce labor costs, and the unions to free up more money for current wages. As a result, many of the plans have gone for years promising benefits without setting aside enough money to pay for them.

The new legislation does nothing to change that dynamic.”

It’s still unclear how this relief effort will work from a practical perspective as the PBGC has 120 days to issue regulations implementing the MEPP provisions signed into law.

Some key details were prescribed in the legislation, as laid out by ABC general counsel Littler’s March 11 analysis of the bill, but many questions of interest to MEPP participants, retirees, employer participants and taxpayers will be answered in forthcoming regulations:

- Which specific plans are eligible for funding?

- What is the ultimate cost to taxpayers?

- Will Congress pass additional structural reforms to MEPPs to prevent a future bailout and limit taxpayer exposure?

- Do MEPP participant employers benefit from current or future withdrawal liability changes if a plan receives taxpayer-funded relief?

MEPPs and the Construction Industry

All MEPPs are defined by the Taft-Hartley Act of 1947. Typically, construction industry contractors that have signed a collective bargaining agreement with a building trades union(s) pay into a trade-specific MEPP fund that is managed jointly by trustees from the specific trade union and select representatives from employers signatory to that union. MEPPs provide defined retirement benefits to participating workers who have met vesting schedules and other requirements during their career.

In general, unionized construction firms use a defined benefit MEPP retirement model while nonunion contractors typically provide defined contribution plans such as a portable 401(k) retirement plan.

“Nonunion contractors are extremely cautious about contributing to MEPPs because it can expose their business to future unknown pension liabilities, and many MEPPs are unlikely to help construction workers achieve their retirement goals,” said ABC Vice President of Regulatory, Labor and State Affairs Ben Brubeck. “They know the MEPP model is flawed and the risks to companies and beneficiaries are just too great to participate and prefer utilizing alternative retirement vehicles.”

Signs of a flawed MEPP system were evident prior to the great recession more than 10 years ago, which put many contractors participating in MEPPs out of business and exacerbated the problem. These contractors failed to pay their share of liability to a MEPP, creating additional liability for a MEPP’s remaining employer participants, which caused insurmountable financial burdens on contributing employers and/or forced the PBGC to take over the plan and cut benefits.

According to data from the PBGC, the construction industry remains a major contributor to current MEPP underfunding and future PBGC MEPP insurance program funding shortfalls and insolvency:

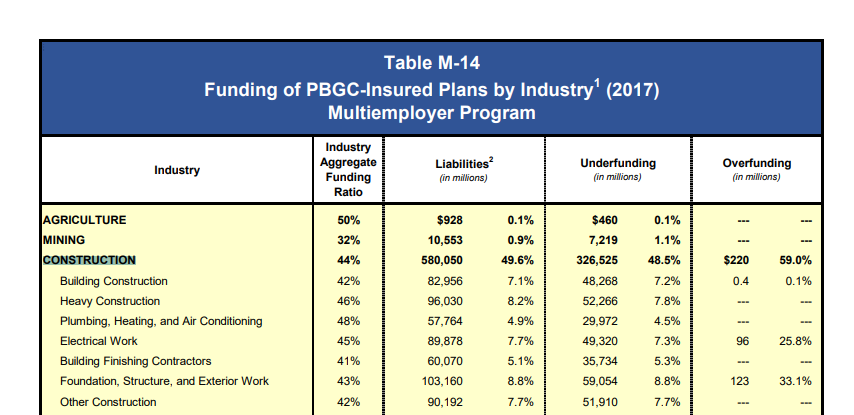

- According to the PBGC’s 2018 Pension Insurance Data Tables, which contains the most recent PBGC data on industry MEPPs, construction industry MEPPs are responsible for about $326.52 billion (or 48.5%) of all PBGC-insured MEPP underfunding, which totals $672.98 billion. (See Table M-14: Funding of PBGC-Insured Plans by Industry (2017) Multiemployer Program).

- The amount of the construction industry’s MEPP underfunding has ballooned over the last decade. In comparison, Table M-14 of the 2010 PBGC reportindicates the construction industry’s portion of all PBGC-insured MEPP underfunding grew to $167 billion (or 47%) in 2009.

- The construction industry comprises $580 billion (49.6%) of the PBGC’s total MEPP liabilities.(See Table M-14: Funding of PBGC-Insured Plans by Industry (2017) Multiemployer Program).

- 755 (55%) of the 1,374 MEPPs insured by the PBGC are in the construction industry. (See Table M-8: PBGC-Insured Plans and Participants by Industry (2017) Multiemployer Program).

- The largest number of employees from any industry, almost 3.877 million (36.7%) of the 10.565 million PBGC-insured MEPP participants (workers and retirees), is from the construction industry. (See Table M-8: PBGC-Insured Plans and Participants by Industry (2017) Multiemployer Program).

Multiemployer Pension Plans and Government-Mandated PLAs

Lawmakers have pushed construction industry contractors and workers into MEPPs via so-called responsible contractor laws and government-mandated PLAs on taxpayer-funded construction projects that can expose contractors to MEPP liability and harm retirement prospects for its workforce.

PLA mandates are a bad deal for hardworking taxpayers and the construction industry because PLA mandates increase construction costs by 12% to 20%, rig the bidding process to discourage experienced nonunion and some union contractors and their qualified workforce from competing to build transformational taxpayer-funded projects and deny good-paying, local jobs to more than 87% of the U.S. construction industry workers who chose not to affiliate with unions.

Problematic terms in government-mandated PLAs discourage competition from union and nonunion contractors and result in a rigged bidding process that forces contractors to:

- Use designated union hiring halls to obtain most or all workers instead of their existing workforce.

- Obtain apprentices exclusively from union apprenticeship programs.

- Follow inefficient union work rules.

- Pay into union benefit and multi-employer pension plans that any limited number of nonunion employees permitted on the project will be unlikely to access unless they join a union and vest in these plans.

- Require their existing workforce to accept union representation, pay union dues and/or join a union as a condition of employment on a PLA jobsite and receive benefits, including MEPP benefits,

An October 2009 report by St. Louis University accounting professor Dr. John R. McGowan, “The Discriminatory Impact of Union Fringe Benefit Requirements on Nonunion Workers Under Government-mandated Project Labor Agreements,” found nonunion workers’ take-home pay is reduced by at least 20% when their employers enter into PLA arrangements containing a MEPP requirement.

In short, nonunion workers participating on PLA contracts can result in a windfall for MEPPs at the expense of workers.

For these reasons, nonunion contractors are typically wary of competing for taxpayer-funded construction contracts that are subject to government-mandated PLAs.

Often a primary concern of contractors deciding to participate on a PLA project is the financial viability of MEPPs, which they would be required to pay into during the life of the project and which could expose their businesses to potentially catastrophic MEPP liability. Information about the health of construction industry MEPPs provided by the U.S. Department of Labor bears out those concerns.

Federal law requires trustees of financially distressed MEPPs in Critical and Declining Status, Critical Status or Endangered Status to provide notice about the level of financial distress to plan participants, beneficiaries, the bargaining parties, the Pension Benefit Guaranty Corp. and the DOL no later than 120 days after the close of the plan year.

Thirty out of 65 MEPPs sending Critical and Declining Status Notices to plan participants in 2020 (reflecting plan performance through the end of 2019) were from the construction industry, according to a list posted by DOL’s Employee Benefits Security Administration.

In addition, 81 out of 121 MEPPs sending Critical Status Notices and 47 out of 61 sending Endangered Status Notices were from the construction industry.

“Lawmakers should not be forcing construction workers and businesses into a broken and flawed MEPP scheme at the urging of their political benefactors,” said Brubeck. “If lawmakers were aware of the health of troubled union-affiliated MEPPs, and the high likelihood of wage theft nonunion workers experience on PLA projects, they might be less likely to require government-mandated PLAs and so-called responsible contracting policies that mandate participation in MEPPs on taxpayer-funded construction projects.”

“Because troubled MEPP notices are not posted on the DOL website in real time, they do not reflect plan performance in 2020, which will be impacted by the volatile stock market returns, a decline in construction spending in some states and localities, and the loss of a record 975,000 construction industry jobs in April 2020 caused by the COVID-19 pandemic,” said Brubeck. “While the industry has gained about 75% back of the lost jobs to date and economists expect the economy to improve once the pandemic is under control, beneficiaries should remain vigilant about the financial health of MEPPs and promised benefits, and contractors should investigate hidden MEPP liabilities that could financially harm a business.”

“The provisions in the COVID-19 relief bill signed into law make it unclear if employers participating in bailed-out MEPPs will receive withdrawal liability relief,” said Brubeck. “While the cash infusion is good news for plan participants, the true cost of this bailout may be much greater than anticipated. Congress failed to address the root cause of the problem, which is the flawed structure of MEPPs. Without future meaningful reforms, there is a strong chance MEPPs and the PBGC will be asking for another taxpayer bailout.”

ABC will continue to monitor all legislative proposals concerning the PBGC and MEPPs and will continue to oppose government-mandated PLAs and other laws mandating contractor and employee participation in MEPPs.

Construction industry stakeholders interested in reviewing construction industry MEPPs in critical and declining, critical and endangered status from 2008 to March 16, 2021, can search this spreadsheet or visit the DOL website on MEPPs.

One Response to Taxpayer Bailout of Multiemployer Pension Plans and Government-mandated Project Labor Agreements

😂complicated topic. No. None. Zero. That is the number of pensions that should be supported/propped up with taxpayer dollars. That includes government pensions. What will the legislators do. They will support the funding because they will be paid off. Probably legally but they will be paid off. This topic will get little attention.