Many Construction Industry Multiemployer Pension Plans Remain Severely Underfunded

Construction unions attempt to entice merit shop craft professionals and young workers into joining a union with promises of generous retirement benefits through multi-employer pension plans (MEPPs).

They also convince elected officials in charge of procuring taxpayer-funded construction projects why union contractors and union workers deserve special treatment through various schemes like government-mandated project labor agreements (PLAs) because of the alleged public good provided by union-affiliated MEPPs. However, data continues to show that many union-affiliated construction industry MEPPs are in serious financial trouble.

The Employee Retirement Income Security Act of 1974 requires the Pension Benefit Guaranty Corporation (PBGC)—a federal agency that monitors and insures pension benefits in private sector defined benefit plans—to provide a report to Congress every five years on the status of PBGC insurance of MEPPs across all industries.

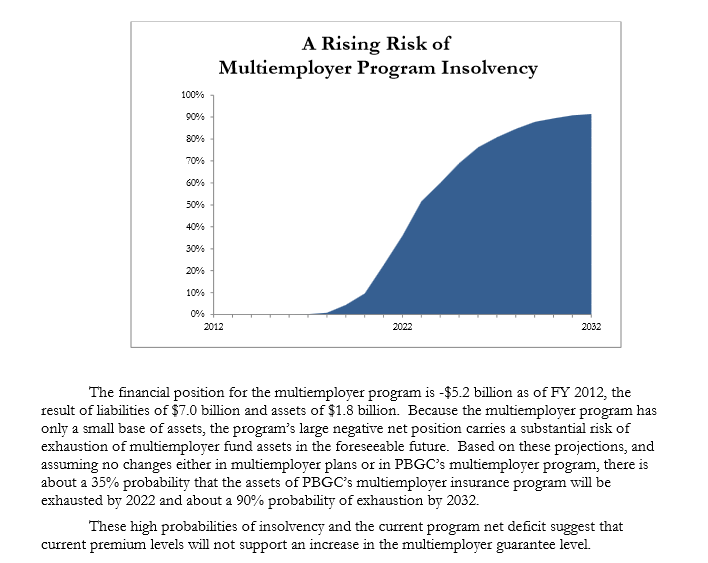

The PBGC’s January 2013 report to Congress confirms MEPPs are distressed:

Construction Industry MEPPs Are Troubled

Additional data from the PBGC indicates the construction industry is a key contributor to the drastic overall underfunding of MEPPs, and a likely cause of dramatic future PBGC insurance program funding shortfalls:

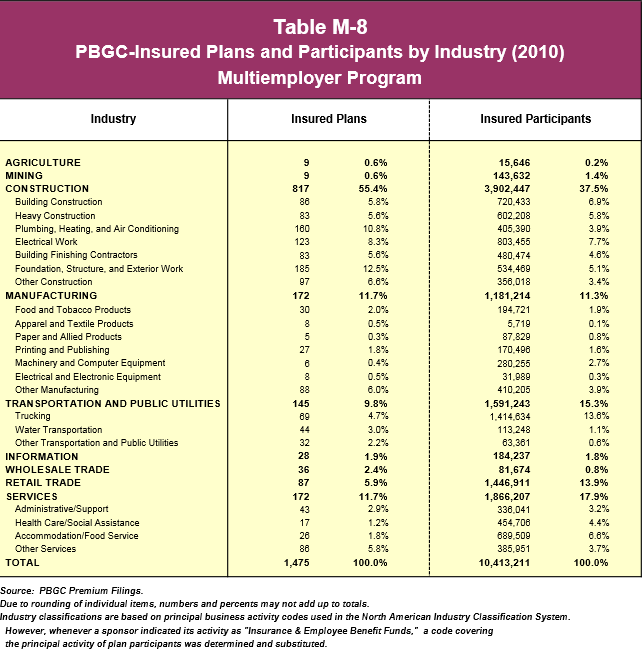

- Fifty-five percent of the 1,475 MEPPs insured by the PBGC are in the construction industry, according to the most recent PBGC report (see table M-8: PBGC-Insured Plans and Participants by Industry (2010) Multiemployer Program).

- The largest number of employees from any industry, about 3.902 million (37.5 percent), of all PBGC-insured MEPP participants (workers and retirees), is from the construction industry.

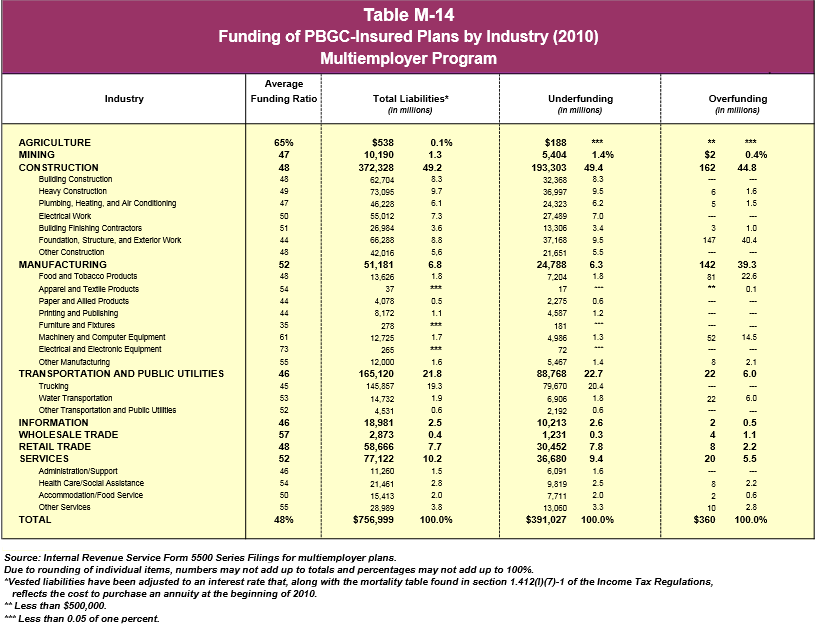

- The construction industry has a total of $372.328 billion (49.2 percent) worth of the PBGC’s total liabilities.

- Construction industry MEPPs are responsible for about $193.3 billion (or 49.4 percent) worth of all PBGC-insured MEPP underfunding (see Table M-14: Funding of PBGC-Insured Plans by Industry (2009) Multiemployer Program).

- In 2009, the PBGC reported the construction industry was responsible for about $87.8 billion (or 45 percent) worth of PBGC-insured MEPP underfunding (see Table M-14: Funding of PBGC-Insured Plans by Industry (2007) Multiemployer Program). Last year’s PBGC report indicated the construction industry’s portion of all PBGC-insured MEPP underfunding ballooned to $167 billion (or 47 percent).

Expect the construction industry’s MEPP underfunding problem to get worse. The industry will continue to be a major contributor to the threat of future PBGC insolvency. Unfortunately, the public still doesn’t know the real-time financial implications of underfunding in 2011 and 2012 thanks to a two-year lag in the public reporting of the health of MEPPs.

Will the MEPP Crisis Result in a Taxpayer Bailout?

The PBGC has publicly raised concerns about the simmering funding crisis because its balance sheet is impacted by the health of MEPPs. MEPP insolvency triggers the PBGC’s guarantee, and loans are provided to the MEPP by the PBGC to help it pay guaranteed benefits (up to $12,870 per year per individual beneficiary). PBGC financing comes from insurance premiums paid by companies insured by the PBGC, as well as other sources such as investment income, plan assets and other recoveries. Taxes do not fund the PBGC plans.

A March 2013 U.S. Government Accountability Office report, Private Pensions: Timely Action Needed to Address Impending Multiemployer Plan Insolvencies, dives into the problems with MEPPs and the PBGC. In short, someday the MEPP funding crisis will impact the solvency of the PBGC. Should the PBGC insurance program become insolvent, one possible solution is a taxpayer bailout of the PBGC and/or many MEPPs.

The National Coordinating Committee for Multiemployer Plans (NCCMP), a consortium of labor unions and MEPP participants, released a paper in Feb. 2013, available at SolutionsNotBailouts.com, offering some possible solutions to the MEPP crisis. Congress is examining the NCPPPs recommendations but it is unknown if they will be adopted. Because related legislation has not been publicly released, it is unclear if the eventual solution(s) will involve a taxpayer subsidy or bailout.

A proposed taxpayer bailout via legislation wouldn’t be unprecedented. In the 112th Congress, Sen. Robert Casey (D-Pa.) proposed legislation described in this Aug. 15, 2010, Wall Street Journal editorial as a taxpayer bailout of the PBGC and MEPPs. So did Reps. Patrick Tiberi (R-Ohio) and Earl Pomeroy (D-N.D.), according to this RealClearMarkets column by Diana Furchtgott-Roth, former chief economist of the U.S. Department of Labor.

MEPPs in the Construction Industry

All MEPPs are defined by the Taft-Hartley Act of 1947 and cover workers from more than one employer. Employer contributions, determined by collective bargaining with a labor union, fund the plan. These plans exist to provide benefits to unionized workers in businesses characterized by frequent job and employer switching, such as union craftspeople in the construction industry. Under a plan, service with multiple employers is treated the same as if the worker had been with the same employer during the life of his or her career.

Unionized contractors receive craft labor from union hiring halls composed of tradespeople who specialize in a specific craft (e.g., IBEW dispatches electricians and LiUNA dispatches laborers). During their career, union workers may be dispatched by union halls to dozens of union-signatory contractor employers. Designated union bosses and union contractors administer pension plans (plan trustees) that multiple union-signatory employers (contractors) must pay into on behalf of employed trade union members in accordance with their respective collective bargaining agreement(s) with a construction union.

In contrast, merit shop contractors typically hire, train and invest resources in tradespeople who work exclusively for the company in a traditional employee/employer relationship. These contractors typically provide benefits packages including a portable 401(k), paid time off, medical and dental insurance, training and profit sharing to attract and retain skilled, experienced employees.

Merit Shop Dislike for MEPPs Justified

As TheTruthAboutPLAs.com has stated many times, one of the reasons nonunion contractors are discouraged from competing for taxpayer-funded contracts on construction projects subject to government-mandated PLAs is because of typical provisions in a PLA that require employers to contribute to union-affiliated MEPPs on behalf of employees for the life of the project.

In rare instances when nonunion employees (and union employees who do not belong to unions that are favored in PLAs) and their employers participate in PLA projects, employers must make hourly benefit contributions to Big Labor’s MEPPs on behalf of their employees. These benefit contributions are forfeited to the MEPP unless employees join a union and meet vesting schedules defined by each plan.

An October 2009 report by Dr. John R. McGowan, “The Discriminatory Impact of Union Fringe Benefit Requirements on Nonunion Workers Under Government-Mandated Project Labor Agreements,” found that employees of nonunion contractors forced to perform work under government-mandated PLAs suffer a reduction in their take-home pay that is conservatively estimated at 20 percent.

Besides stealing benefits rightfully earned by construction employees working on a PLA project, PLA pension provisions are a windfall for Big Labor’s MEPPs because the MEPPs don’t have to pay future benefits to those employees. Though small in comparison to overall funding shortfalls, these contributions prop up insolvent plans and hide the flawed structure and Ponzi-scheme economics of many construction industry MEPPs.

For decades, merit shop firms have offered alternative retirement plans to their workforce because union-affiliated MEPPs simply cannot be financially sustained in the long term. Construction industry stakeholders have only recently publicly addressed MEPP underfunding, partially because of scrutiny from the financial industry.

For example, data from Moody’s Global Corporate Finance’s Sept. 10, 2009, report, “Growing Multiemployer Pension Funding Shortfall Is an Increasing Credit Concern,” measured the crisis faced by construction industry MEPPs. Using 2007 numbers as a starting point, Moody’s estimates that 2008 underfundings for construction MEPPs ballooned to $72.484 billion, or a 54 percent funded level. In other words, for every dollar that these construction MEPPs owe, they hold only 54 cents of invested assets.

With unemployment in the construction industry at 10.3 percent as of May 2010 and the industry’s real unemployment rate in the high teens, it is no surprise that contractors (specifically union contractors) that participate in these MEPPs are going out of business. And when MEPP participants go belly up, the burden on employers remaining in the MEPPs becomes greater. Bankrupt contractors that can’t pay their fair share to MEPPs create additional liability for a MEPP’s remaining employer participants, which results in all sorts of disastrous consequences, such as forcing more employers out of business, weakening already struggling MEPPs, compelling the PBGC to step in, which could trigger PBGC and MEPP insolvency.

The Blame Game

The recession, a decline in construction industry union membership, a high industry unemployment rate, industry demographic changes and a looming construction industry workforce shortage point to future insolvency for many MEPPs.

In response, Big Labor has tried to exploit its political clout to fix its pension woes by pushing lawmakers and unelected bureaucrats at the National Labor Relations Board to pass rules that will make it easier for unions to organize and add new members to the basement of their MEPP scheme (see the Employee Free Choice Act/Card Check, Executive Order 13502, Ambush Elections, Micro Unions and Invasion of Privacy).

In addition, unions have ratcheted up rhetoric blaming their pension troubles on Wall Street and the recession. Instead of pushing reasonable solutions like adjusting benefits, increasing contributions, preventing fraud and waste, executing sound investment and management strategies, and diverting hundreds of millions of dollars of discretionary union political spending to pension plans, unions are playing the blame game and posturing for a bailout from Uncle Sam. The union MEPP crisis is a key reason why unions hijacked the recent Occupy Wall Street movement and trumpeted this loaded question: If Wall Street can get a bailout, why shouldn’t union pension plans?

However, the shaky financial condition of some MEPPs was obvious pre-recession and occurred under the watch of union pension trustees, such as this example from a TheTruthAboutPLAs post:

The Sheet Metal Workers National Pension fund discloses the plan’s annual funding levels for plan participants here. The SMWIA union’s own pension fund documents indicate that on 1/1/2008, the fund was just 52.2 percent funded.

So just three months after the Dow closed at an all-time high of 14,164 on 10/9/07, the pension fund took such a big loss in the stock market that the plan ended the year at 52.2 percent funded? Something doesn’t smell right.

This July 26, 2009, WSJ article points to similar anecdotes of pre-recession MEPP underfunding in other industries, as well as inequality between the pension plans of rank-and-file members and Big Labor bosses:

Poor management probably deserves a lot of the blame for the union decline, but the exact causes are a mystery. An even bigger mystery is that the unions do a far better job with funds created for their officers and employees than for mere workers. The SEIU Affiliates, Officers and Employees Pension Plan—which covers the staff and bosses at its locals—was funded as of 2007 at 102.2%. The plan for the folks at SEIU international headquarters was funded at 84.8%.

A September 2009 report on union pension plans by the Hudson Institute, “Comparing Union-Sponsored and Private Pension Plans: How Safe Are Workers’ Retirements?” found similar results and highlighted the disparities between union officer pension plans and union member plans. So does this piece.

Get to Know Your MEPP

The U.S. Department of Labor provides a list of all MEPPs in the critical and endangered status here. We’ve sorted through the growing list and identified construction industry MEPPs in this easy-to-search spreadsheet. Check to see if the MEPP you are participating in (or that your competitors pay into) is in trouble.

For too long, construction industry employees, contractors and lawmakers have been fooled into thinking union MEPPs deserve special treatment, are without fault and are a safe retirement strategy. The truth is that many plans are not in good shape and haven’t been healthy even in the best of economic times. Construction industry MEPPs have offered little transparency, accountability or meaningful solutions. Without proper education, oversight and corrective action, workers, contractors and taxpayers should expect more of the same.

Share your thoughts, concerns and anecdotes on this issue in the comments section.

Required Reading

- Multiemployer Pension Plans Face Uncertain Future (pdf)

- A Hitchhiker’s Guide to Taft-Hartley (pdf)

- “The Union Pension Bomb: Multi-employer plans look to be in big trouble,” WSJ, 5/14/12

- “The Multiheaded Pension Monster,” WSJ, 4/23/12

- “US Union Pensions Hole Deepens To $369 Billion,” Financial Times, 4/8/12

- “Crawling Out of the Shadows: Shining a Light on Multiemployer Pension,” Credit Suisse, 3/26/12

- “The Next Pension Bailout,” WSJ, 8/15/10 (pdf)

- Spreadsheet of construction industry MEPPs in critical or endangered status (Updated July 2013)

TheTruthAboutPLAs.com posts on MEPPs:

- The Dismal Future of Construction Industry Multiemployer Pension Plans, 4/23/12

- New Report Finds PLA Pension Requirements Steal From Employee Paychecks, Harm Employers and Taxpayers, 10/24/09

- Construction Union Pension Plans and Project Labor Agreements, 9/11/09

- Construction Unions Push PLAs to Save Underfunded Union Pension Plans, 6/10/09

- Construction Unions Posture for Pension Bailout?, 7/30/09

Readers can keyword search “pensions” to review the numerous posts TheTruthAboutPLAs.com has written about the link between government-mandated PLAs and MEPPs.

3 Responses to Many Construction Industry Multiemployer Pension Plans Remain Severely Underfunded

[…] Read Full Article Here […]

I suggest if you are construction worker to not join a union because the you can be under paid and work in a sweat shop.

[…] million workers, retirees and family members. By far the largest portion is in the construction industry. It’s not hard to see why. Multiemployer plans offer something that single-employer plans […]